When “Free” Advice Costs You $1.5 Million in Healthcare Spend

Kirk Conole • April 24, 2026

For many businesses, healthcare is one of the largest and fastest-growing expenses on the balance sheet. Yet the way most companies manage it hasn’t changed in decades.

A recent case we worked on highlights just how costly that can be.

The Situation

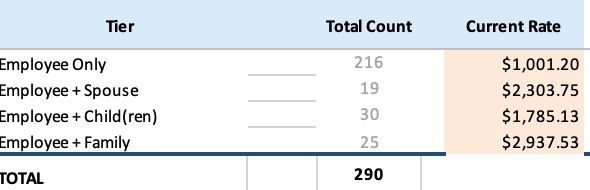

A company with 290 employees

received their renewal from Blue Cross Blue Shield.

The projected increase: 16.99%

That pushed their expected annual healthcare spend to approximately:

👉 $5.5 million

For a group of this size, that number should raise eyebrows.

But unfortunately, it’s becoming more common, not less.

Why This Keeps Happening

Most employers rely on their broker to:

- Shop the market

- Negotiate rates

- Present plan options

And to be fair, most brokers are

doing those things.

The issue is how

they’re doing them.

In a traditional fully insured model, “shopping” typically means moving between the same handful of carriers:

- Blue Cross Blue Shield

- UnitedHealthcare

- Aetna

- Cigna

Each year becomes a cycle:

- Receive a large increase

- Shop the market

- Shift carriers or adjust plans

- Repeat next year

This approach may create the appearance

of cost control, but it rarely produces meaningful, long-term savings.

The Real Problem: A Reactive Strategy

The traditional model is reactive by design.

Employers are:

- Responding to renewals instead of controlling them

- Accepting trend increases as unavoidable

- Operating with limited visibility into what’s driving costs

Without transparency and a proactive strategy, costs will continue to rise, regardless of how often the plan is “shopped.”

A Different Approach

Instead of simply remarketing the plan, we helped this client rethink their healthcare strategy entirely.

By implementing a more strategic and data-driven approach, we were able to:

👉 Reduce total annual healthcare spend from $5.5 million to $4 million

That’s a $1.5 million reduction, achieved without cutting benefits or shifting additional burden to employees.

So… Is Your Broker Really “Free”?

Many employers believe their broker services come at no cost.

Technically, that’s true; there’s no direct invoice.

But broker compensation is typically built into your premiums.

Which means:

If your current approach results in millions of dollars in unnecessary spend…

you’re still paying for it, just indirectly.

The Cost of Staying the Same

If your organization is:

- Experiencing annual increases of 10% or more

- Remaining fully insured without exploring alternatives

- Relying solely on market “shopping”

There’s a strong chance you’re overpaying for healthcare.

And over time, those incremental increases compound into millions.

A Better Question to Ask

Instead of asking:

“Did we shop the market this year?”

Consider asking:

“Do we have a strategy to control our healthcare costs long-term?”

That shift in thinking is where real savings begin.

A Final Thought

Healthcare costs don’t rise because employers aren’t trying hard enough.

They rise because most are operating within a system that wasn’t designed to control them.

If your projected spend is approaching $5M+ for a 300-employee group, it may be time to rethink the strategy, not just the carrier.

Let's Talk

At DCI Solutions, we help companies take a more strategic approach to healthcare — one that prioritizes transparency, control, and measurable savings.

If you’re questioning your current trajectory, we’re happy to have a conversation.

The fewer copper phone lines that exist, the more expensive they become. For decades, Plain Old Telephone Service (POTS) lines were the backbone of business communications. They powered fax machines, alarm systems, elevators, fire panels, point-of-sale terminals, and countless other mission-critical devices. Today, they're rapidly disappearing. Yet many organizations continue paying for legacy copper lines they no longer need, or paying dramatically inflated prices for the ones they still do. The result? Thousands of dollars in unnecessary telecom spending, hiding in plain sight.

Many construction firms assume the best way to lower insurance costs is to shop their coverage to as many carriers as possible. In reality, that approach often produces the same result: multiple quotes based on the same flawed assumptions, inflated values, and standard market pricing. Recently, a builder reduced construction insurance premiums by more than $1 million without a traditional shopping exercise. The savings came from restructuring the program before it ever reached underwriting.

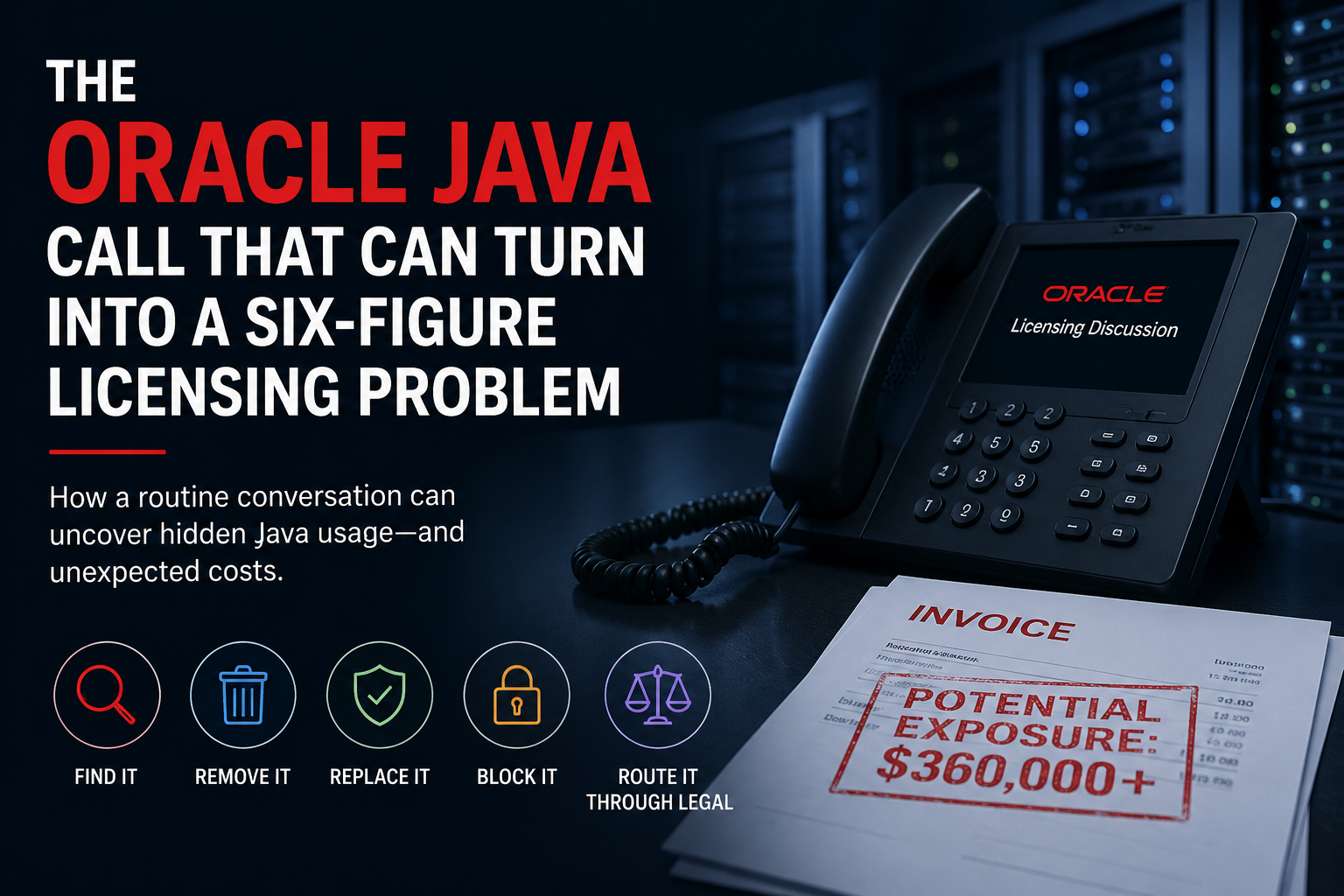

For many IT leaders, it starts with what sounds like a routine phone call. Oracle reaches out requesting a "quick discussion" about your Java environment. The conversation is typically positioned as a support check-in, a licensing update, a security discussion, or a general review of your organization's Java usage. On the surface, it appears harmless. In reality, the discussion often serves a much different purpose: determining whether Oracle Java exists anywhere within your environment. Once that is established, the conversation tends to shift quickly. Questions may include: How many employees does your organization have? Who is using Oracle Java? Which systems rely on it? Are contractors or subsidiaries involved? How broadly is Java deployed across the enterprise? At that point, the licensing exposure calculation begins.

Many employers who hire blue-collar workers assume they're receiving every available Work Opportunity Tax Credit (WOTC). The reality is that many companies lose valuable tax credits simply because the process isn't being monitored correctly. One of the easiest ways to verify compliance is through a monthly reporting system. A simple report should clearly show: New hires screened on time Missed forms Late submissions Overall compliance percentage In the example below, the employer achieved: 100% of new hires screened on time 0 missed forms 0 late forms That level of compliance helps ensure tax credits are protected and available when it's time to file. The problem is that many organizations never receive this type of visibility. Without regular reporting, missed screenings and late paperwork can quietly eliminate tax credits that should have been captured. The financial impact can be significant. Even a relatively small number of qualified hires may generate thousands of dollars in tax savings. In many cases, companies discover additional opportunities through an independent audit of their tax credit and operational processes. A thorough forensic review often uncovers overlooked savings, compliance gaps, and process inefficiencies. For many organizations, the combined effect can translate into meaningful cash flow improvements without changing vendors, disrupting operations, or taking on additional risk. The question isn't whether WOTC credits exist for your workforce. The question is whether you're capturing every dollar you're entitled to. When was the last time an outside expert reviewed your process? Being busy is understandable. Leaving money on the table isn't.

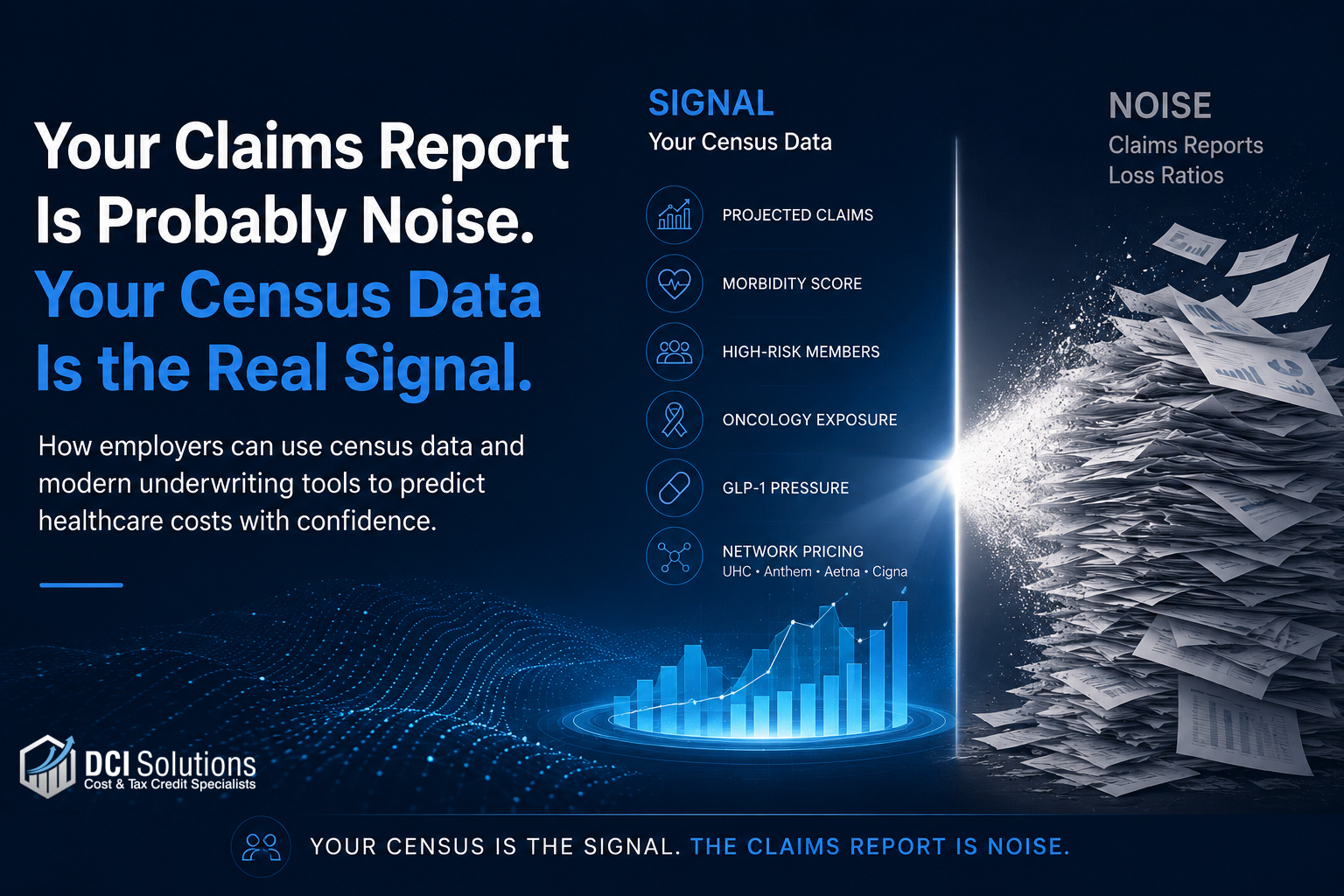

For decades, employers have been conditioned to believe that health insurance claims reports are the key to understanding healthcare costs. They're not. In fact, by the time most employers receive a claims report, the information is already historical. It tells you what happened, not what's likely to happen next. That's a problem when healthcare spending continues to rise and employers are being asked to make critical decisions about funding strategies, stop-loss coverage, network selection, and employee benefits.

Learn how high performance standards reveal hidden savings in your business. Contact DCI Solutions for expert cost management today!

Learn how a private college cut elevator maintenance costs by 70%, saving $185,000 annually. Contact DCI Solutions for effective strategies.

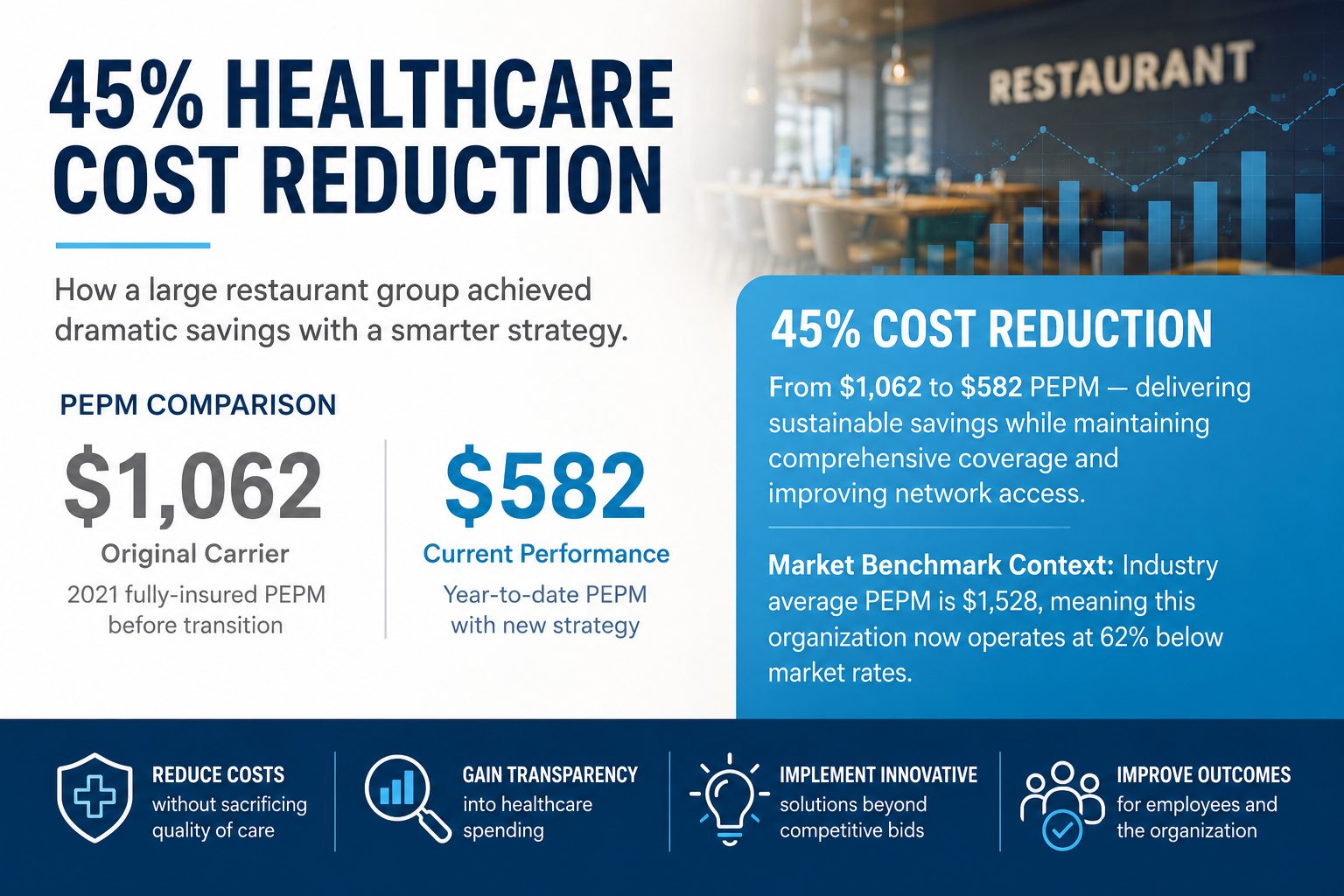

Learn how a restaurant group cut healthcare costs by 45% using self-funding & AI analytics. Contact us to explore similar savings!

Most companies accept annual freight increases as unavoidable. FedEx Freight’s LTL general rate increased 5.9% from 2023 to 2024, and then another 5.9% from 2024 to 2025. Over time, these annual General Rate Increases (GRIs) quietly compound into a major expense line that most businesses never fully challenge. But what if you could reverse the impact of those increases?

Employers can unlock federal tax credits by hiring student employees. Contact DCI Solutions to maximize your savings today!